Before we begin, the word “Miles” in this article refers to credit card miles or points. The word “Cashback” refers to credit card cash back or cash rebates.

Value

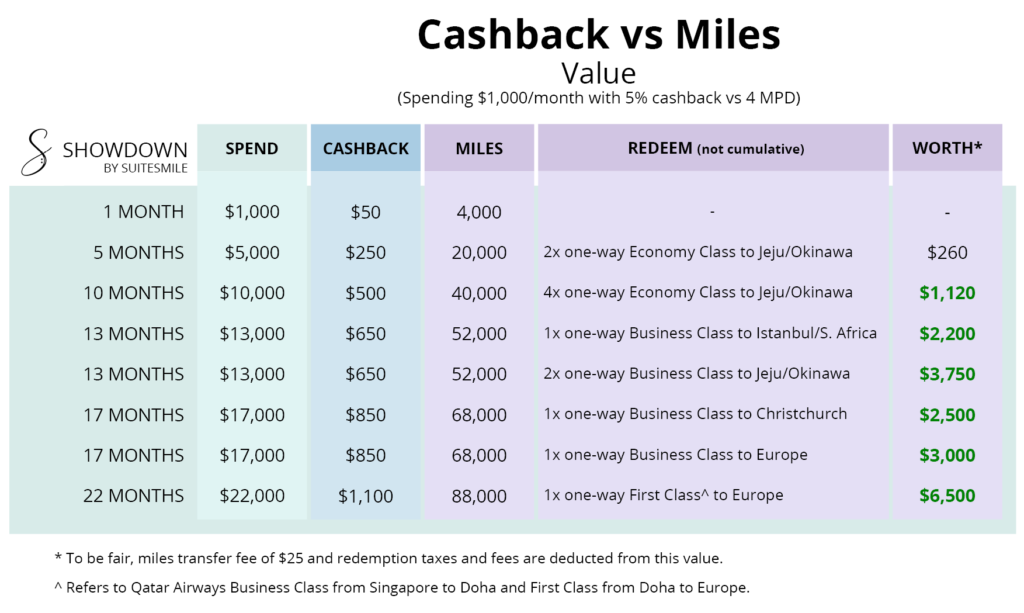

Let’s start off with the most important factor, value.

In this comparison, let’s take a look at how much value a person can get if he spends an average of $1,000 monthly. Let’s also make the fair assumption that he can either earn 5% cashback OR 4 miles per dollar (MPD) from the entire $1,000 every month.

The fruits of your labour takes a little longer when you use Miles cards. After 22 months, you will get 6 times more value with Miles cards than Cashback cards. No contest in this category.

Common Myth 1

“I have to be a big spender to earn enough miles to redeem for flights.”This is not true. Even with a monthly spending of $200, you will have enough miles to fly to Japan in about one year. You just need to use the right cards.

Common Myth 2

“I have a family of 4. It will take forever to earn enough miles to take my family on vacation.”The table above should put this myth to bed. Sure, it may take longer to redeem your miles for flights in a premium seat. But you will definitely get better value with Miles cards even if you are the only spender in the family.

Winner: Miles

| Subscribe to Suitesmile on Telegram to be the first to know about amazing deals and travel hacks. It's FREE! |

| Subscribe |

Minimum spending

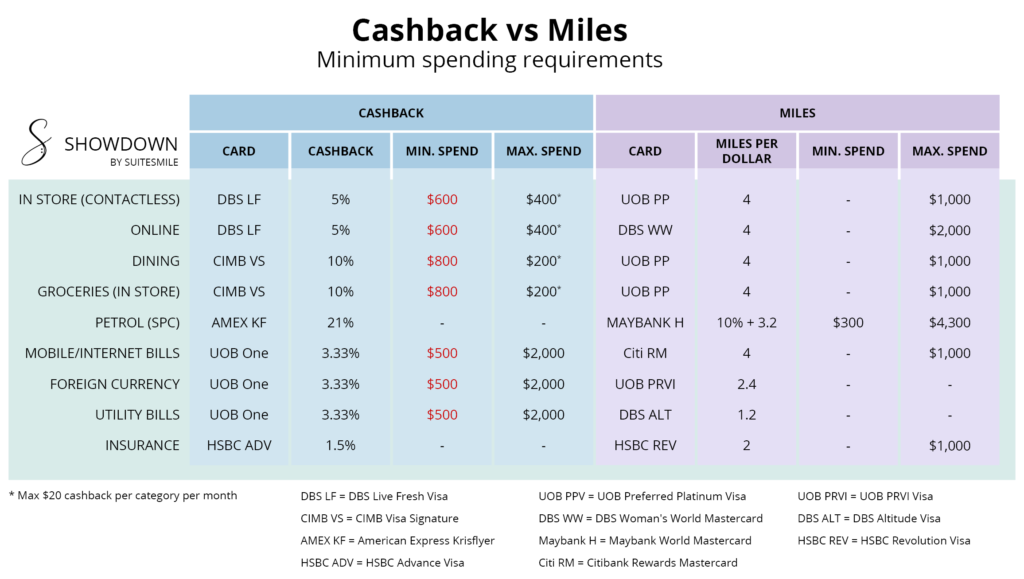

Let’s take a quick look at the best cashback and miles cards for each spend category and the minimum spend required to achieve the headlining cashback or earn rate.

There are many Cashback cards that offer similar cashback rates and minimum spending requirements. The cards listed above were picked based on my opinion on which ones have a good balance of cashback and spending requirement. That said, it would be so much easier to use UOB One for everything other than Insurance. With this card, you will earn a little lesser cashback but only one minimum spending to worry about.

But hey, does it matter? Miles cards do not require any minimum spending.

Winner: Miles

Expiry

Miles expire, most of the time. From the cards listed in Table 2, most expire 2 years from the dates they are earned. This does not mean that you have to redeem for a flight within 2 years. With good planning, you can transfer these expiring miles to a preferred Frequent Flyer Program (FFP) when the miles are close to their expiry dates.

If you transfer them to Singapore Airlines Krisflyer, they will expire 3 years later, hence, giving all your miles an effective validity period of 5 years (2 with the bank + 3 with Krisflyer).

The better option, in my opinion, is transferring your miles to Cathay Pacific Asia Miles. Asia Miles do not expire as long as there is at least one activity in your account within an 18 months period. This is extremely easy to achieve with a simple $10 purchase from iHerb via iShop or a 1,080 miles donation to UNICEF. Because of how easy it is to extend the validity of your miles, you can take your time in accumulating them for a dream flight with 5-star airlines like Cathay Pacific, Qatar Airways and Japan Airlines.

Cashback does not expire, of course. They get credited to your card and you can spend it off in the coming months.

Winner: Cashback

Devaluation

Award charts of FFPs all over the world go through devaluation cycles every few years. Most of the time, the amount of miles required for the same destination will increase by a little bit. This means that if you are new to miles accumulation, you may be hit by a devaluation before your first miles redemption. Although a small devaluation does not take away the fact that Miles cards can give you about 6 times more value than Cashback cards, cash does not devalue. Well actually it does but you will be able to spend your cashback so fast that you will not feel it.

Winner: Cashback

One card strategy

As mentioned above, it is easy to choose one Cashback card. UOB One card offers 3.33% cashback for monthly spending of $500 – $1,999. You will need to spend this amount for 3 consecutive months to qualify. Hitting $2,000 for 3 consecutive months will give you 5% cashback (max $100 a month).

Choosing one Miles card is trickier. The common mistake that most newbies make is picking a general spending card that gives them a measly 1.4 MPD. Instead, a better pick would have been the UOB Preferred Platinum that gives you 4 MPD on contactless payments and some online spending.

Using the above example of $1,000 monthly spending, even if having one Miles card only give you 4 MPD for half of your monthly spending, you will still come out on top. Looking at Table 1 above, you can get as much as 6 times more value as compared to a Cashback card.

Keeping track of multiple credit cards requires a bit of effort but is very easy with our free tools. If you haven’t, read about how to drastically minimize the risk of accumulating credit card debt.

Winner: Miles

Difficulty

These are the things that you have to do with each card type:

Cashback

Remember which card to use for each category

Track minimum spending

Miles

Remember which card to use for each category

Have a redemption plan

Track expiry of miles in each card or bank

Find out award sweet spots for a high value redemption

Search for award flight availability before redeeming your miles

Transfer miles to desired frequent flyer program (usually with a fee of around $25)

To maximize your miles accumulation and redemption value, quite a bit of work is required. Using our free spreadsheet makes it a whole lot easier.

Winner: Cashback

| Subscribe to Suitesmile on Telegram to be the first to know about amazing deals and travel hacks. It's FREE! |

| Subscribe |

Mix & Match

Although I am using miles cards for most of my spending, let me remind you that there is absolutely no reason to pick a “team”. Contrary to popular belief, there is no Cashback or Miles God that will put you in heaven if you stay devoted to each side. There is one category from my list of the best credit cards in Singapore where Cashback wins hands down; that is petrol spending at SPC. To keep things less complicated, I value 4 MPD as an equivalent of 7.6% cashback. When I see a Cashback card that offers more than this number, I would choose it over a Miles card that offers 4 MPD.

The winner

The ultimate winner is pretty clear, Miles. In most cases, I should say. However, there are situations where you should pick Cashback cards over Miles cards. They are:

If you don’t care about value.

If you absolutely hate travelling or flying.

If you do not have 30 minutes to learn the basics of the Miles game.

Conclusion

Banks and airlines do not like mile-savvy people like you. They want you to burn your miles on microwave ovens or for an upgrade to a really old Business Class seat on your next 2-hour flight to Bangkok. But if you are willing to put in that extra bit of effort in learning the “Miles game”, the value that you can get out of your day-to-day spending is spectacular.

Follow us on Telegram, Instagram and Facebook to receive our latest updates.